Note from Sean: When Julie sent me an email asking if she could write a post for freelancers all about how to manage finances that included topics like taxes, figuring net worth, paying off debt, and how to make a budget, I was all for it.

Figuring out your finances both before you start freelancing and as you get into it is really important and something that’s probably not talked about enough. With this post, Julie covers a ton of super valuable information.

Take it away, Julie!

—

Can I quit yet? How much do I need to be earning before I quit? Does my new income need to match my day job income before I quit, or is there another measure? How much do I need to save before I quit? How will I know for sure when I can quit?

If any of these questions sound familiar, you’re in the right place!

When I first found Location Rebel’s precursor, Location 180, I thought, I want that! I wanted the freedom to live and travel on my own terms. A lot of us start our own businesses to make that happen. These businesses allow us to quit our day jobs.

The question is, when can you actually quit that day job?

By the end of this post, you’ll have the answers you’re looking for.

Whether you already have a new business going and you’re hoping to quit your current job tomorrow or you haven’t even thought about what side job to start yet, it’s ok.

In this post, I’m going to help you create a specific plan for saving and earning so that you know exactly what needs to happen for you personally to be able to leave your job and run your own business.

Ready to get started? Let’s jump in!

First, start with your goals

The first step is always to set goals.

In this case, your goal is probably to quit your current job, or maybe to scale back your hours. There are 3 main ways to do this. None are “right” or “wrong,” it’s just a matter of which feels most comfortable to you. Choose one now, and remember, you can change your mind later if you need to. Do you want to:

- Quit your current job before you have any new business, and you will hustle to get a business going after you quit?

- Quit your current job when you have a new business that looks promising but doesn’t cover all of your expenses yet?

- Wait to quit your current job until your new business covers all of your necessary expenses?

By the end of this post you will have a better idea of how each of these options will play out, but for now, keep in the back of your mind whichever one of these makes your gut say “Yes! That’s the one!”

Taxes, insurance, and business expenses – oh my!

Before we get down to the good stuff, I want to be clear what this post is and what it is not. This is all about your personal budget, and how much profit you need to have in your new business in order to support yourself.

We won’t be discussing business expenses because those are, well, expenses in your business.

We’re only concerned with your business’ profits. If your business has revenue of $10,000 per month and the business expenses and taxes add up to $8000 per month, then you can’t spend $10,000 on personal expenses and savings; you have $2000 for personal expenses and savings.

If you want to know more about business finances, check this out.

We also won’t be talking about taxes. Keep in mind, though, that in the U.S. you can expect your tax situation to change when you own your own business, so figure out what your tax rate will be and account for it. Put money aside for taxes throughout the year (or pay estimateds if you’re in the U.S.) so you don’t get caught in a jam next spring.

And then there’s insurance. If you’re not in the U.S., you might roll your eyes here. Yes, many of us lose important benefits when we quit our jobs. I’ll cover this later.

Join over 40,000 people who have taken our 6 part freelance writing course. Sign up below and let’s do this together.

By entering your email address you agree to receive emails from Location Rebel. We'll respect your privacy and you can unsubscribe at any time.

Where do you stand?

Before you know how much money you will need to quit your current job, you need to know what you’ve got right now. To keep it short, I’m covering the necessities here and I have included links to some of my posts if you want more detail. These steps are all actionable, so let’s go take some action!

Before we dive in, a quick heads’ up: money is emotional.

Sometimes that’s obvious, like when we shop to relieve stress. And sometimes it catches us off guard, like when we work through the steps in a post like this and feel overwhelmed, guilty, or embarrassed.

Just remember: by this time tomorrow, you will know exactly what you’re numbers are to make things happen. So it’s totally worth it!

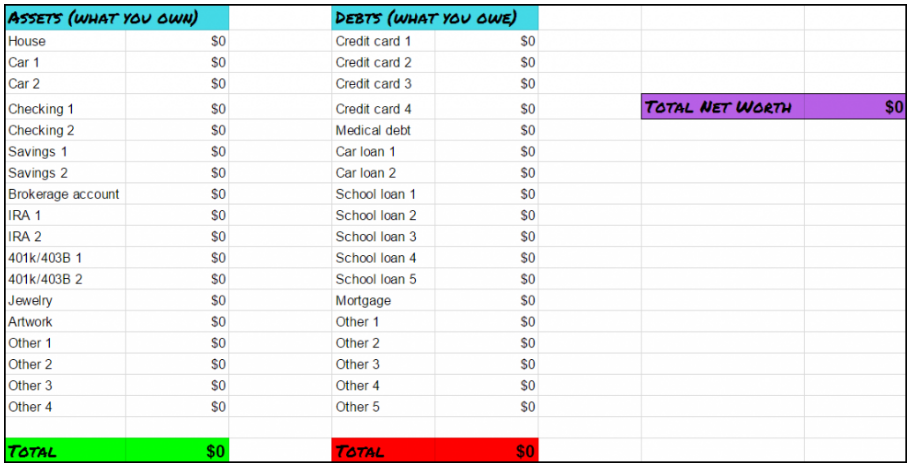

What’s your net worth?

Your net worth is what you own minus what you owe (your assets minus your debts.) Add categories as needed to the chart below. Then fill in your amounts and add up each column.

Finally, subtract your debts from what you own. You can also get this chart as a free calculator (no email required) to do the math for you.

Remember that disclaimer about things getting emotional?

Sometimes this is super fun and sometimes it totally sucks. Either way, don’t get discouraged because I will be giving you steps to improve your net worth. For now, it’s enough to know your current net worth.

What’s your current income?

Simply list all of your income sources. If you get $50 each month for watching your neighbor’s dog when they travel, put it in. If you earn $100 each month selling your stuff online, put that in. It will all be relevant. I give more details on my budgeting approach here.

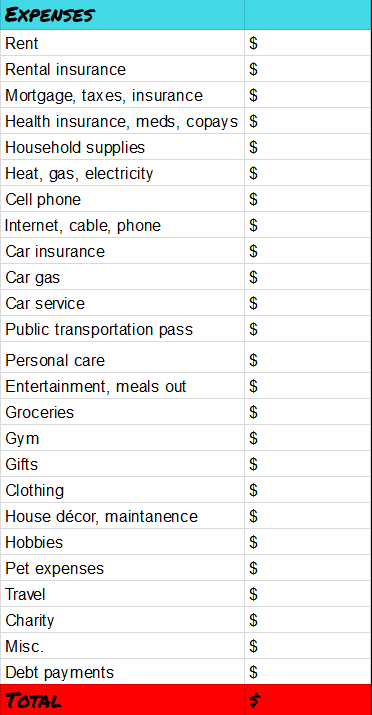

What are your current expenses?

This is a hard one. Sometimes we have no clue what we spend. Other times we think we know our spending, but we’re wrong.

I have worked with many clients, and no one has been right about what they spend unless they track it (including me!). Tracking your spending is the best way to get exact data, but that takes time, and I want you to have answers today.

So instead, here’s your do-it-in-a-day shortcut:

- Gather your credit card, debit card, and bank statements from the last 12 months.

- Make a chart like the one below, and list out your spending categories.

- For every expense on your statements, put it into one of the categories. Make up new categories as needed.

- Do not say, “This is a one-time thing, so it’s not important.” The reason we’re doing 12 months of expenses is that there’s always going to be an “unusual” expense and we want to catch them. Maybe this year it’s a new mattress and next year it’s a major car repair and then a few months later your drop your phone in the toilet. It’s better to be prepared for these things. Feel free to have a “Usual Expenses” category, if that’s easier.

- Add up your total expenses in each category. Divide this number by 12 to see how much you spend in that category on average each month.

- Add up all of these totals to see your total average monthly spending.

That looks like a lot, but it can be done in an afternoon. I have done it with my clients. It might get emotional again, but push through, because it will be very worth it.

What you know now

Yesterday, did you know your net worth, your current income, and your current expenses broken down by category? Probably not, but now you do! Congratulations!

Give yourself a big pat on the back (or for me, some celebratory chocolate), because now you know a lot more about your money than just about anyone else knows about their money. That means you’re ready to take things to the next level.

Crush your debt for big success

Most people have debt. When you calculated your net worth, did you have anything in the debt column? When you added up how much you spend every month, how much of that was for debt payments?

Your goal is to have more freedom, right? Isn’t that the whole point of quitting your day job – to live life on your own terms? Debt holds us back from that. So it’s important to get rid of it. I know it feels impossible and scary, but it’s doable.

You’re going to start doing that right now.

Step #1: Stop making new debt. This means you need to stop spending more than you earn. This is necessary before you quit your current job.

Step #2: Get current on all debt. If anything is in collections or otherwise delinquent, address it.

Step #3: Pay off credit card debt first. Choose the smallest bill, and throw as much money as you can at it as you follow the steps below. Make minimum payments on the rest of your debts. Once that card is paid off, throw as much money as you can at the next smallest card. Once all of your credit cards are paid off, move on to medical debt and your car loan (more on getting rid of car loans later.) Then chip away at your school loans. The mortgage will wait for now.

Many people think, why put a lot of money into paying their debts when they could use that money for something more fun, to fund their business, or simply to have extra savings in the bank?

I understand that temptation, but let me ask you: how much are you paying towards debt every month? Now, what would you do if you had that extra money available to you?

A client just paid off a lot of debt and now has an extra $900 every. single. month. That gives him a ton of options. If you didn’t have debt payments every month, wouldn’t that make it a lot easier to save up to quit your job?

You’re going to pay that debt eventually. You can pay the balances now, or you can pay them over time, with interest. Interest payments can add up to more than the original purchase!

Also, right now your new business might need to cover $4000 in expenses, but when pay off your debt and get rid of those monthly payments it will only need to cover $3000 in expenses. That’s a big difference for a new business. And, if your business has a lower income month, you won’t need to stress out about those debts.

Remember, your goal here is freedom.

You will have a lot more freedom when you’re not in debt.

Calculating your new Goal Minimum Income

Eventually, you want to be earning enough profit in your new business to cover all of your necessary expenses, a bunch of frivolous expenses, and lots of savings. That’s a fantastic future goal, but that’s not today’s goal. You will be quitting your job before your reach that point.

At the beginning, you simply need to cover your most necessary expenses. I call this your Goal Minimum Income (GMI.)

Go back to your chart of expenses from the past 12 months. Mark off the categories that will go away or be reduced after you quit your job.

For example, if you wear suits to work every day and your new life will be one of jeans and sweatshirts, you can eliminate your dry cleaning category. Be careful to be realistic.

If you eat out for lunch every day because you never have time to prepare food to bring to work, it’s great to think you will stop eating lunch out altogether. But will you have lunch meetings for your new business? Will you use it as a chance to get out of the house and be social?

Once you mark off all of the categories that will be reduced or eliminated, make a list of new categories. Remember, we’re only talking about personal expenses here, not business expenses.

Maybe you won’t be buying work clothes anymore, but now you need clothes for the new climates you will be traveling to. If you’re planning to travel the world, add in those travel expenses. If you’re going to start new hobbies, add those in.

Estimate realistic amounts for each category. And of course, add in health insurance costs. These change often, but go online right now to get a current estimate.

Now, take your new list of expenses and prioritize it.

There’s a saying in personal finance: you can have anything, but you can’t have everything. When you first quit your job, some things might be beyond your budget for a while.

Which things are you willing to give up for 6-12 months? Which are non-negotiable?

Again, be realistic. The easiest way to fail is to plan to give something up because you think you should, even though you know in your heart that you won’t.

I’m not judging you for your choices here – they’re YOUR choices, so make sure they work for YOU! If you want to quit your day job asap even if it means giving up your favorite activities for a while, then go for it. If you would rather work at your job for another year so that you don’t have to give up those favorite activities, that’s totally cool. This is another area where emotions like to get in the way, so watch out for them.

Being honest with yourself is how you will be happy and successful when you do quit.

Once you determine your non-negotiable expenses that you must have for the first 6-12 months, add them up. Take this total, and add a cushion to it because you Just. Never. Know. Life happens. How big the cushion needs to depend on your comfort level and your savings.

Start with a cushion of 10% and adjust it according to your comfort. If your total is $2700, you might add a 10% cushion and then round it up to $3000.

This is your Goal Minimum Income (GMI).

When your business earns this amount steadily each month, you will be paying all of your necessary bills. As your income goes up, you can add in more of your luxury expenses and start saving.

Building your Quit-My-Job Savings before you quit

Knowing your Goal Minimum Income is a huge piece of the puzzle. The next piece is how much you should have in savings before you quit.

In 2009 I quit a job where I was unhappy. It was the height of the Great Recession and all around me were stressed out people. I, on the other hand, was having the best time. I hadn’t been out of work since I was a teenager, and I was loving it! I didn’t even look for work for the first 6 months. I just needed a break.

How did I do this?

Simple: I didn’t have any debt, and I had savings. With no debt hanging over my head, I had more freedom. And with enough savings, (and knowing my GMI) I knew exactly how long I could pay my bills and be out of work.

Savings gives you huge amounts of freedom! It’s time for you to build up savings so you can quit your job and enjoy your own freedom. Let’s call this your Quit-My-Job Savings.

How much you need to save will depend on several things, including which of the three quitting approaches at the start of this post most appeals to you.

Maybe you’ve heard the conventional wisdom that you should have 3-6 months’ worth of expenses in an emergency fund. That’s a wise approach when someone has a steady income, but we’re talking about you quitting your steady income for something less steady.

That means you need to think differently. You should have Quit-My-Job Savings in addition to your emergency fund.

Ask yourself these questions:

- If your business doesn’t provide the income you need, what will you do? Will you try another business? Will you get another 9-5 job?

- How long will you keep at your new business before you give up? Would you wait 6 months? Two years?

These answers will partially determine how much you need to save.

The other part of the equation is your income.

Remember those three scenarios we started with? Which one are you aiming for? If you plan to quit your job before you start a new business, you will need a lot more saved up than if you have a business that’s already covering most of your expenses before you quit.

For example, let’s say your Goal Minimum Income (GMI) is $3000 per month:

- If you plan to quit your job before you have a new business, and you want to give yourself a year to meet your GMI, then you need at least $36,000 ($3000 x 12 months = $36,000) in savings before you quit.

- If you plan to have partial income from your new business before you quit, then you won’t need to have quite as much saved up. If you aim for $2000 per month in income, then you need to make up the other $1000 from savings, and if you plan to give it a year, then you should have $12,000 ($1000 x 12 months = $12,000) saved up.

- On the other hand, if you plan to have your new business provide the full $3000 per month before you quit your job, then you don’t need any additional savings.

Why bother with an emergency fund?

Now, you might ask why you need to have these savings in addition to an emergency fund. Why not just save $36,000 as in the first example here and let that be your emergency fund, too?

Well, that’s because they serve different purposes. What if you get into a car accident and the repair will cost $6000? If you take that from your Quit-My-Job Savings, then you just lost 2 months that you could have spent working on your business.

On the other hand, if you have an emergency fund, you will pay for car repairs from that and your Quit-My-Job Savings will still sustain you for 12 months. Emergency funds handle emergencies so that your Quit-My-Job Savings can support your regular expenses after you quit your job. They give you peace of mind.

And if you end up not needing all of your Quit-My-Job Savings? Then you will have extra money to travel, buy a house, invest in your business, etc. Having extra savings is a great “problem” to have! You do this so you can avoid the real problem of running out of savings.

Hint: If you find motivation in having no savings, if you crave that sense of urgency you get from being broke and having to hustle for your income, then put your savings in a place that’s hard to access. One option is to put it in an account in an online bank with no ATM card and no checkbook. You can still get at the money in an emergency, but it will be hard enough to get to that you’ll have that sense of urgency.

Finding YOUR Quit-My-Job numbers

That was a lot. Are you still with me? Take a deep breath, because it’s about to get a lot easier and more fun. It’s finally time to figure out when you can quit your job!

Step #1: Pick Your Approach

Choose one of the approaches I outlined at the start, and get into more detail.

- If you want to quit your day job before you’ve started a new business, what will your planning level be? Will you already know what your new business will be? Have you signed up for a course to learn more? Will you be starting from scratch?

- If you will have a partial income from your new business before you quit your day job, how much will that income be? 25% of your GMI? 50%? 80%?

- If you want your new business income to cover your GMI before you quit your day job, how many consecutive months should this happen before you feel confident in the trend? Obviously, 1 month is not enough, what about 4 months? Or 6 months?

Be specific.

Example: I am conservative, so I want my new business to earn 80% of my GMI for 6 consecutive months before I quit my current job.

Step #2: Your Goal Minimum Income

You calculated your GMI earlier. Go back to your list of expenses and double check, then triple check them.

Are they realistic? Are you planning any cuts that make you cringe? Have you included all of your likely new expenses? Are you comfortable with the cushion you added?

Apply your GMI to your approach from Step #1.

Fill in the blanks: “My GMI is $______. Before I quit my job, my new business needs to provide ____% of my GMI for ____ consecutive months. This is $_____ per month for ____ months.”

Example: “My GMI is $3000. Before I quit my job, my new business needs to provide 80% of my GMI for 6 consecutive months. This is $2400 per month for 6 months.”

Step #3: Your Quit-My-Job Savings Goal

Look at the percentage of GMI that your Quit-My-Job Savings needs to cover every month when you first quit your job.

Do the math to figure out the dollars. Then multiply it by how long you are planning to work at your new business before you reach your GMI (or move on to something else.) Fill in the blanks:

“My savings needs to cover ____% of my GMI which is $______ every month. (Hint: this number is your total GMI minus the amount in Step #2.) I need this to last for _____ months after I quit which means I must save $_______ (the amount per month x the number of months.)”

Example: “My savings needs to cover 20% of my GMI which is $600 every month. (Total GMI $3000 and business will be earning $2400 so $3000 – $2400 = $600) I need this to last for 12 months after I quit which means I must save $7200 (because $600 x 12 months = $7200)”

This is the amount you need to save up in addition to your emergency fund, after your credit cards and car loan are paid off and your school loans and mortgage are in good standing.

Step #4: Reaching Your Quit-My-Job Numbers

Time to make this happen!

I just laid out all of the information you need. Now you know when you can quit your day job: when your business reaches the income in Step #2 and your Quit-My-Job Savings reaches the amount in Step #3. I could end this post right here, but I want to give you a few ways to accelerate Q-Day’s arrival.

Accelerant #1: Increase income

Paying off debt and building up savings goes faster when you have more income. If your new business is already bringing in profit and you’re still working a full time day job, then throw your new business’s profit into paying off debt first and then building up your Quit-My-Job Savings.

Beyond this, get creative.

Sell things around the house that you don’t need. Consider selling bigger things. Can you sell your car? Sean did this, and it worked out great. Notice this can also get rid of your car loan! Can you get a roommate? What about babysitting or dog walking? Only you know if these things are worth it so that you can finally quit your day job. Choose 1 thing for now and go for it.

Accelerant #2: Cut expenses

Most people cringe at this suggestion, but cutting even 1 monthly expense does 3 things for you:

- It gives you extra money to put into paying off debt and Quit-My-Job Savings.

- It lowers your GMI. Now you don’t need to earn as much from your new business! If your GMI is $3000 and you want to cover 80% of that before you quit, you need $2400. If you cut just $300, your new GMI is $2700 and 80% of that is $2160.

- Because your GMI is lower, your Quit-My-Job Savings can be lower, too. Let’s say your GMI is $3000. To cover 20% of that for a year, you need $7200. Now let’s say you cut $300 of expenses from your budget and your new GMI is $2700. To cover 20% of that for a year you only need $6480. The more you cut, the less you need to save.

Some monthly expenses to cut or reduce would be cable, subscriptions you don’t need or use, gym memberships, and overpriced cell phone plans.

If you sold your car in Accelerant #1, you just saved money on car payments, insurance, gas, and service. Review your credit and debit card bills, circle anything that is billed monthly, and consider ways to cut or reduce them. After you make these changes, redo the math for your GMI and your Quit-My-Job Savings. Enjoy the new lower goals!

And it’s not only about monthly expenses! One time expenses really add up, too. Every time you go out to dinner, every time you want to buy new clothes or a book, every time you’re tempted by some random purchase or drinks out with friends, ask yourself 1 question:

“Would I rather have/do this, or would I rather quit my job sooner?”

If the answer is that you’d rather quit your job, then skip that purchase and instead put the money into your Quit-My-Job Savings. If you would rather have or do that thing, go for it! Now you’re making an informed choice. The goal here is to pay attention to where you spend your money and to not spend it mindlessly.

Accelerant #3: Rinse and Repeat

It’s tempting to do everything above and then walk away. That’s easy, but it’s not the most effective. Review your income, spending, and savings at least once a month. As you become more aware of your money, you will notice yourself making unconscious improvements.

In addition, every time you do a review, consider new ways to increase income and cut expenses. Your standards and goals will change subtly over time, and you will probably find yourself wanting to make changes next month that you’re not ready for today.

Outlining your timeline to quit

I could write a book about your timeline, but we’ll have to be content with this shortcut.

After doing everything above, you should have an idea of how much money you can save every month. Use that amount to figure out how long it will take you to pay off each credit card, your car loan, etc. This calculator will help you figure it out, taking interest rates into account. You can also play around with the effect that making above-minimum payments will have.

Remember, each time one debt is paid off, take the monthly payments you were making and put them towards the next debt you plan to pay off. For example, if you are paying $500 per month towards one card and $200 per month towards another, and you pay off the larger one first, then your new monthly payments for the next card will be $700 per month. This new, larger payment allows you to pay it off a lot faster than you otherwise would.

Once your debts are gone, take those monthly debt payments and put them into your Quit-My-Job Savings.

Simple math will tell you when that will be fully funded: $______ (needed Quit-My-Job Savings) / $_______ (currently monthly savings) = ______(months remaining).

For example, if you need $7200 and you already have $2,000, then you need additional Quit-My-Job Savings of $5200. If you’re saving $850 per month, then $5200/$850 = 6.1 months.

Add the number of months you will need to pay off your debt and the number of months you will need to build up your Quit-My-Job Savings.

Once your debts are gone and your Quit-My-Job Savings are in place, all that’s left is for your business income to meet the percentage of your GMI that you committed to. Calculating your business income is beyond scope of this post (what, you want this to be even longer?!) If you can meet that income level by the time your debt is paid off and your Quit-My-Job Savings is funded, you’ll be ready to quit that day!

Julie Morgenlender is a Financial Freedom Coach, working with women to end their money stress and become money-EMPOWERED instead. She works with women to pay off debt, build up savings, take control of their money, and fund their dreams. She blogs at juliemorgenlender.com. She also enjoys knitting, crochet, reading just about any genre of book, writing a book of her own, and cuddling with all of the neighborhood dogs. Because dogs!

Disclaimer: All of the content in this post is the author’s opinion and thought. It’s accuracy and completeness are not guaranteed. None of the advice, opinions, or suggestions offered here are meant to be followed without consideration for your own personal circumstances. They are offered as something for you to think about. This isn’t specific financial advice. It is information. When the author responds to comments, those are her thoughts and opinions based on limited information. You are responsible for your own actions.

Guest Post

Join over 40,000 people who have taken our 6 part freelance writing course. Sign up below and let’s do this together.

By entering your email address you agree to receive emails from Location Rebel. We'll respect your privacy and you can unsubscribe at any time.

Solid financial advice! I run through this with my students when they start talking about quitting their job to freelance full time.

By the time we get through this they realize they should wait six months, double their revenue and pay down their bills.

It is amazing how simple exercises like this bring such startling clarity.

Great work.

Thank you so much Jesse! I’m glad to hear you run through this with your students regularly. I hate to think of people quitting their jobs to freelance full time without being prepared financially – it will lead to so much stress and a higher rate of failure. It’s good they get to benefit from your wisdom!

The timing on this post could not have been more perfect!! Exactly what I needed. I’m on the threshold of leaving my job, I have a few months to figure it out and, with this post, I’m off to a confident start. Thank you Julie for the step-by-step guide as well as the encouragement to muster through. And thank you Sean for guesting Julie on your blog. Great stuff all round!

That’s great Lainey! Congratulations on making the leap! I’m glad the timing worked out so well for you. If it gave you confidence and a strong approach, then it did its job. If you have any questions about your own situation, please hit me up!

Julie, that’s by far the best article I’ve read on the subject. Excellent for referral/curation. I’ve bookmarked the article for my new site.

Thanks Annie! I’m so glad you’ve found it helpful. Let me know if there’s anything else you’d like to know!